Anúncios

Managing your personal finances is not just about saving money, it’s about building stability and freedom. In today’s fast-paced digital economy, where online shopping, credit cards, and subscription models make it easy to overspend, understanding how to organize your finances has become a vital life skill.

Many people feel overwhelmed by bills, debts, or the complexity of financial planning, but with structure and consistency, anyone can regain control. Whether you’re saving for retirement, managing student loans, or trying to live within your means, financial organization is the foundation of long-term success.

This article will guide you through seven effective steps to organize your personal finances in 2025, combining practical strategies, digital tools, and mindset shifts that can truly transform your relationship with money.

Step 1: Set Clear Financial Goals

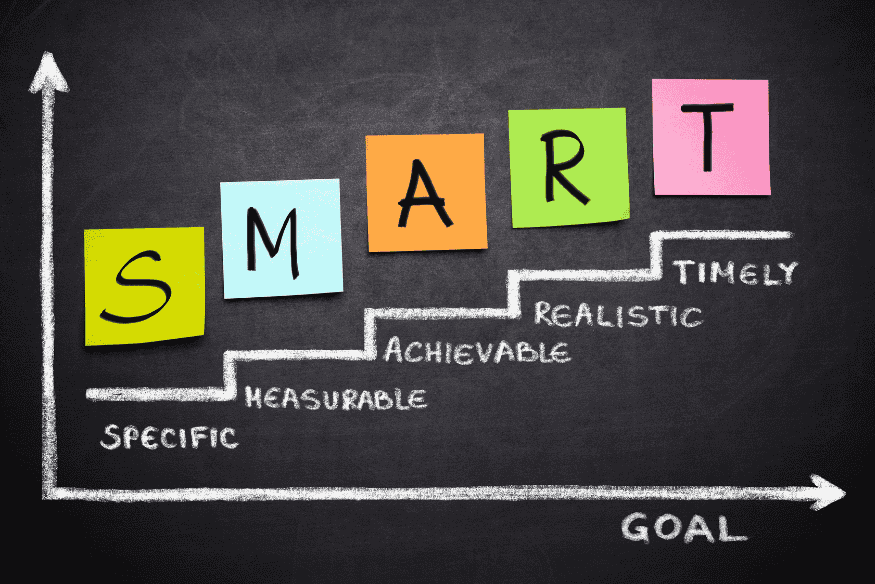

Before you can organize your finances, you need to know what you’re aiming for. Are you saving for a down payment, paying off credit card debt, or preparing for a comfortable retirement? Setting clear goals provides motivation and direction.

Begin by writing down what you want to achieve and when. Divide your objectives into short-term (less than a year), medium-term (one to five years), and long-term (over five years). This categorization helps you visualize progress and stay accountable. For example, a short-term goal could be saving $1,000 for emergencies, while a long-term goal could involve building an investment portfolio for your future.

Use the SMART framework (Specific, Measurable, Achievable, Relevant, and Time-bound) to turn vague dreams into actionable financial plans. Having these goals in writing also helps you track your growth and adjust your strategy when needed.

Step 2: Track Your Income and Expenses

It’s impossible to improve what you don’t measure. Tracking your income and expenses is the backbone of financial awareness. Start by identifying all your income sources, salary, freelance work, passive income, or side hustles. Then, categorize your expenses: housing, transportation, food, insurance, entertainment, and personal care.

Many financial apps like Mint, PocketGuard, or YNAB can automate this process by connecting to your bank accounts and analyzing spending habits in real time. If you prefer a manual approach, a spreadsheet or a notebook works just as well. After one or two months, you’ll see clear patterns of where your money is going. This awareness can be eye-opening, revealing habits like frequent dining out or unused subscriptions.

Differentiate between fixed costs, which stay constant, and variable costs, which fluctuate. Once you know where your money flows, you can make intentional decisions about where to cut back and where to allocate more resources.

Step 3: Build and Maintain a Monthly Budget

Creating a budget transforms financial chaos into clarity. The goal isn’t to restrict your lifestyle but to manage your money consciously. Start by applying the 50/30/20 rule: 50% of income for necessities, 30% for discretionary spending, and 20% for savings or debt repayment. If your financial situation is tight, you might adjust this to 60/20/20 or another ratio that fits your circumstances.

The key is consistency. Tools like Google Sheets or budgeting apps can simplify tracking, but the habit of reviewing your budget monthly is what truly makes the difference. During each review, compare your planned expenses with actual spending and make small tweaks. Budgeting also helps prepare for irregular expenses such as annual insurance premiums or holiday gifts. Over time, it teaches discipline and confidence, ensuring you always know where your money stands.

Step 4: Pay Off Debt Strategically

Debt can feel like a heavy burden, but with the right strategy, you can overcome it systematically. Begin by listing all your debts with details such as outstanding balance, interest rate, and minimum payment. Then, decide between two popular methods:

- The Debt Snowball method focuses on paying off smaller balances first to gain psychological momentum.

- The Debt Avalanche method targets high-interest debts first, saving more money in the long run.

Both approaches are effective; the best one is the one you can stick with. Automate your payments to avoid late fees and protect your credit score. If possible, negotiate lower interest rates or consolidate your debts into a single payment with better terms. Remember, every dollar paid toward debt brings you closer to financial independence. Paying down what you owe frees up income for savings, investments, or simply more peace of mind.

Step 5: Build an Emergency Fund

Financial security begins with preparation. An emergency fund acts as a safety net against unexpected events like job loss, medical emergencies, or urgent repairs. Aim to save at least three to six months of essential living expenses. If that seems daunting, start with a smaller goal, even $500 can make a difference.

Keep your fund in a high-yield savings account that is easily accessible but separate from your regular spending account to avoid temptation. Automate weekly or monthly transfers to make saving effortless. This habit not only builds your fund steadily but also trains you to prioritize financial safety. An emergency fund prevents you from relying on credit cards or loans in times of crisis, ensuring stability even when life throws curveballs your way.

Step 6: Automate Savings and Investments

Automation is one of the smartest tools for long-term financial growth. Once your budget and goals are set, schedule automatic transfers to savings, investment accounts, or retirement funds. This “pay yourself first” approach ensures saving becomes a non-negotiable part of your routine. If your employer offers a 401(k) plan, contribute enough to get the full company match and it’s essentially free money.

Beyond that, consider diversifying into low-cost index funds, ETFs, or IRAs to grow wealth steadily. For those new to investing, robo-advisors like Betterment or Wealthfront offer easy, low-maintenance options. Automation removes emotional decision-making from the equation and helps you build wealth effortlessly over time. As your income increases, adjust your contributions to stay aligned with your goals and inflation.

Step 7: Review and Adjust Regularly

Personal finance is dynamic, not static. Life changes, like new jobs, family responsibilities, or economic shifts, can affect your plan. That’s why regular reviews are crucial. Every few months, evaluate your goals, spending, and investments. Check if your budget still reflects your priorities. Perhaps you can now save more or invest differently.

Review your credit report annually to ensure accuracy and protect against identity theft. Use digital dashboards or apps that visualize your financial growth to stay motivated. Small adjustments can have a big impact over time, keeping your plan realistic and resilient. By developing the habit of reviewing and refining, you ensure that your financial system evolves with you rather than against you.

Conclusion

Organizing your personal finances is one of the most empowering actions you can take. By setting clear goals, tracking income and expenses, budgeting wisely, reducing debt, and automating savings, you lay the groundwork for stability and growth.

Financial control brings freedom, the freedom to make choices based on values, not fear. Start with one step today, however small, and commit to consistency. Over time, these habits will not only transform your bank account but also your peace of mind, leading you toward a secure and confident financial future.