Anúncios

If you have ever looked at your statement and wondered why your balance keeps growing even when you are making payments, you are not alone. Understanding how interest on a credit card is calculated is one of the most important steps to taking control of your finances. With many cards charging high rates in 2025, every dollar you carry from one month to the next can become significantly more expensive over time.

In this guide, you will see what APR actually means, how banks turn that annual rate into a daily charge, how grace periods work, which types of transactions are usually more expensive, and practical strategies to reduce or even avoid interest altogether. The math behind these interest charges is simpler than it looks, and once you understand it, you can make smarter decisions every time you swipe or tap your card.

What Is APR and How Interest on a Credit Card Works

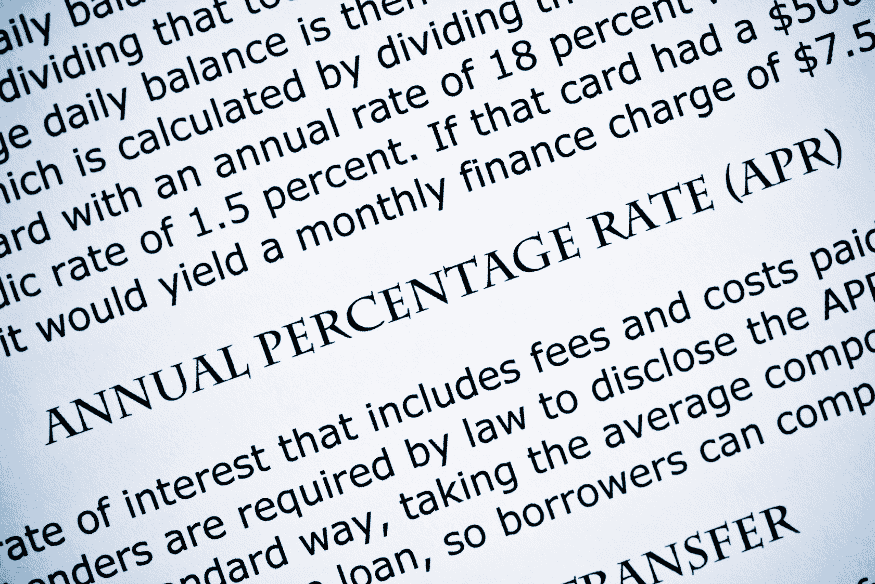

At its core, the credit card interest is the price you pay for borrowing money from your card issuer. Instead of being quoted as a monthly rate, it is expressed as an Annual Percentage Rate (APR). A purchase APR of 20% does not mean you are charged 20% on your balance every month. It describes the yearly cost of carrying debt on your account when you do not pay it off in full.

Most cards use a variable APR, which can move up or down with market interest rates. You may also see different APRs on the same card: one for purchases, another for balance transfers, a higher one for cash advances and sometimes a penalty APR if you miss payments. The APR gives you the headline price, but interest is actually calculated every day based on your balance, which is why small debts can quietly grow into much larger ones if you ignore them.

From APR to Daily Charges: The Math Behind Your Statement

Even though APR is listed as a yearly number, your issuer turns it into a much smaller daily rate to calculate how much credit card interest you owe in each billing cycle. The process usually follows a few clear steps that you can copy with a calculator or spreadsheet.

- First, the bank converts the APR into a daily periodic rate by dividing it by 365. For example, an APR of 21% becomes about 0.0575% per day.

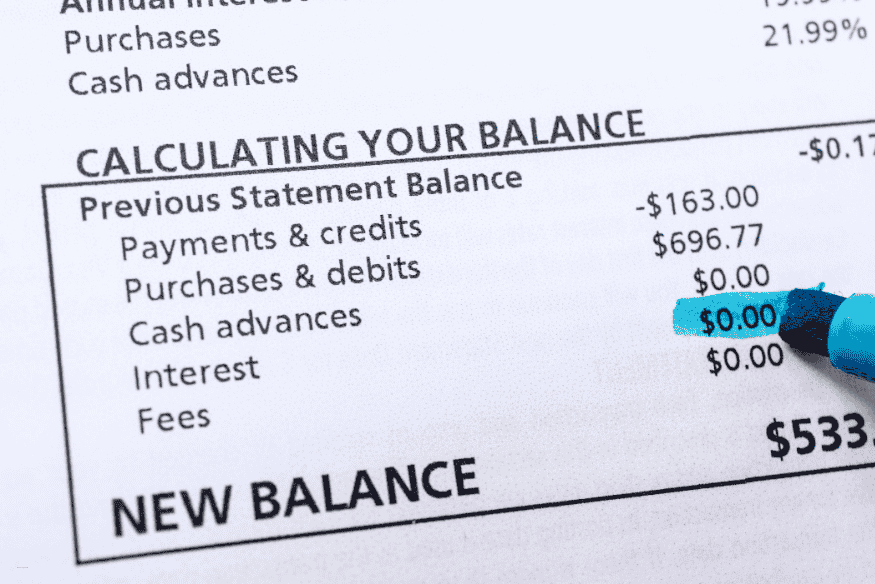

- Then, the issuer tracks your balance every day of the billing cycle, adding new purchases, fees and any unpaid interest and subtracting payments or credits as they post.

- At the end of the cycle, all daily balances are added together and divided by the number of days to find your average daily balance.

- Finally, your interest charge for the month is calculated by multiplying the average daily balance by the daily rate and by the number of days in the cycle.

Imagine your average daily balance is $1,000, your daily rate is 0.0575% and your cycle has 30 days. The interest charge would be 1,000 × 0.000575 × 30, or about $17.25, which is then added to your balance.

Grace Periods and When You Pay No Interest

The most powerful way to avoid paying interest on everyday purchases is to use the grace period correctly. The grace period is the window of time between the end of your billing cycle and the payment due date. If you pay your statement balance in full by that date, you usually do not pay any interest on new purchases from that cycle.

This benefit can disappear if you start carrying a balance. When part of your previous statement balance remains unpaid, many issuers begin charging interest on new purchases from the day they post, rather than giving you an interest-free period. Cash advances and some balance transfers typically never have a grace period at all, which is why they can become expensive very quickly.

Reading your card agreement and your monthly statement helps you understand exactly when interest starts and how to keep your grace period active so you do not unintentionally build up more credit card interest than you expect.

Different Types of Interest on Your Card

Not every transaction on your card is treated the same way, and knowing the difference can help you pay less credit card interest overall. Behind the scenes, your issuer can track several separate balances and apply a different APR to each of them.

- Purchases APR applies to day-to-day spending when you do not pay your statement balance in full.

- Balance transfer APR covers debt you move from another card, sometimes at a promotional 0% rate for a limited time before switching to a higher ongoing APR.

- Cash advance APR is usually much higher, often starts on the day you withdraw money and may be combined with a separate cash advance fee.

- Penalty APR can be triggered by repeated late payments or serious delinquency and can make existing debt much more expensive until your account improves.

By understanding which APR applies to each part of your balance, you can decide which debts to tackle first and which types of transactions to avoid whenever possible, reducing the amount of interest you pay over the long term.

Habits That Reduce How Much Interest You Pay

The math behind these interest charges matters, but your day-to-day behavior matters even more. Two people with the same card and the same APR can end up paying very different amounts over the year depending on how they manage their balances and payments.

The single best habit is to pay your statement balance in full and on time every month so you can keep your grace period and avoid interest on new purchases. When that is not possible, paying more than the minimum and paying earlier in the cycle can still reduce interest by lowering your average daily balance. Avoiding cash advances, watching for rate increases and limiting new purchases while you already carry a balance also help keep your debt from growing.

Creating a payoff plan, such as focusing extra money on the card with the highest APR, turns these individual habits into a strategy that steadily reduces what you owe. Over time, consistent behavior makes a much bigger difference to your total credit card interest than any single month’s payment.

Conclusion

Credit card interest does not have to be mysterious or overwhelming. Once you understand how APR is turned into a daily rate, how your average daily balance is built and how the grace period protects you when you pay in full, your statement becomes much easier to read. From there, small changes in how and when you pay can dramatically cut the amount of interest you give to the bank.

Take a few minutes to look at your next statement, note your APRs and balances and decide how much you can realistically pay above the minimum each month. With a clear view of how credit card interest works and a simple payoff plan, you can move from feeling stuck in revolving debt to using your card as a controlled, useful financial tool.